THE RIGHT COVERAGE.

THE RIGHT

AMOUNT.

Most people have the wrong type of insurance, the wrong amount, or a policy that won't do what they think it will when it matters most. We fix that — with a clear, pressure-free analysis built around your life.

No jargon. No sales pitch. Just honest guidance on what you need — and what you don't.

🛡️ Licensed & Independent Advisor

📋 Personalized Coverage Analysis

💬 Zero Sales Pressure. Ever.

INSURANCE IS CONFUSING BY DESIGN. WE MAKE IT

IMPOSSIBLY SIMPLE.

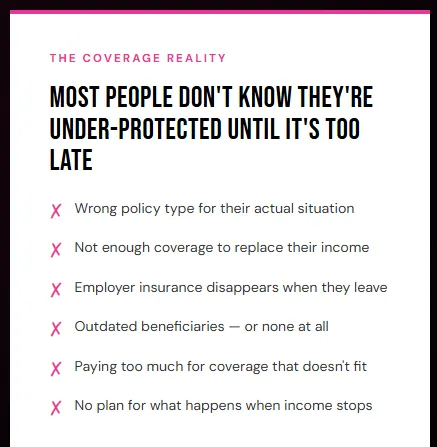

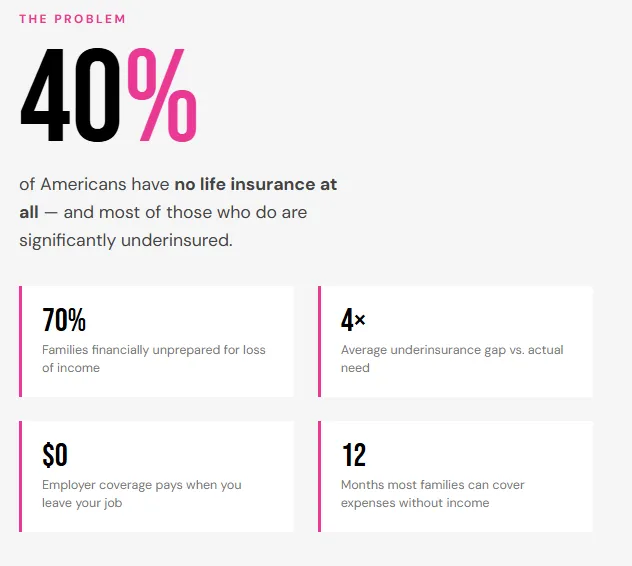

Most people have no idea if their policy actually covers them.

They bought something years ago, have no idea what's in it, and haven't thought about whether it still matches their life. A quick review often reveals gaps — and savings.

Your employer's coverage is a false sense of security.

Group life insurance typically covers 1–2× your salary — a fraction of what your family actually needs. And the moment you leave that job, so does the coverage.

Term vs. Whole vs. IUL isn't a simple answer — it depends on your goals.

The right policy isn't about what sounds good. It's about what fits your income, your family, your retirement timeline, and your legacy goals. That's what we figure out together.

The Framework

THE 3 STAGES OF

INSURANCE PLANNING.

Where you are in life determines what kind of coverage you need. Most people are stuck in stage one — or skipped it entirely. We help you identify your stage and build from there.

BASIC SAFETY NET

START HERE — PROTECT WHAT YOU HAVE NOW

—

If you have a family, a mortgage, or anyone who depends on your income, this is the non-negotiable foundation. The goal is to make sure your people are taken care of if something happens to you.

✓ Replace your income for your family

✓ Pay off debts and the mortgage

✓ Provide immediate family stability

✓ Affordable, essential coverage

COVERAGE OPTIONS

Term Life · Final Expense

STRATEGY + PROTECTION

BUILD LONG-TERM WEALTH WHILE STAYING PROTECTED

—

Once your foundation is solid, insurance can do double duty — protecting your family AND building tax-advantaged cash value you can access in retirement. This is where most people leave significant money on the table.

✓ Grow cash value tax-advantaged

✓ Protect long-term income

✓ Build legacy and generational wealth

✓ Create a tax-free retirement income stream

COVERAGE OPTIONS

Whole Life · Indexed Universal Life (IUL)

SECURE INCOME, PASS WEALTH

LOCK IN INCOME. LEAVE A LEGACY.

—

At this stage, the focus shifts to guaranteed income you can't outlive, protecting what you've built from taxes and long-term care costs, and making sure your legacy passes cleanly to the people you love.

✓ Tax-free legacy transfer

✓ Guaranteed lifetime income

✓ Long-term care protection

✓ Estate planning support

COVERAGE OPTIONS

Whole Life · IUL · Annuities · Final Expense

Not sure which stage you're in? That's what the analysis is for.

Coverage Options

EVERY SOLUTION EXPLAINED SIMPLY.

TERM LIFE INSURANCE

The purest form of income protection. A term policy covers you for a set period — 10, 20, or 30 years — at the lowest possible premium. Ideal for the years when your financial responsibilities are at their highest: young kids, mortgage, building wealth.

Best For

Young families · Mortgage protection · Income replacement · Budget-conscious buyers

WHOLE LIFE INSURANCE

Guaranteed lifelong coverage that builds real cash value you can actually use. Whole life is a financial asset — not just a policy. The cash value grows tax-deferred, can be borrowed against, and is guaranteed never to decrease. A cornerstone of generational wealth planning.

Best For

Long-term wealth building · Estate planning · Business owners · Legacy transfer

INDEXED UNIVERSAL LIFE(IUL)

Permanent coverage with flexible premiums and cash value that participates in market growth — with a floor so you never lose value in a down year. IUL is one of the most powerful tools for building tax-free retirement income alongside life insurance protection.

Best For

Tax-free retirement income · High-income earners · Long-term financial planning · Legacy strategies

FINAL EXPENSE INSURANCE

A small, affordable whole life policy designed to cover funeral costs, medical bills, and end-of-life expenses. No medical exam required. This is about making sure your family doesn't have to scramble financially while they're grieving.

Best For

Ages 50–85 · No medical exam · Fixed premiums · Immediate peace of mind

MORTGAGE PROTECTION

Specifically designed to pay off your mortgage if you pass away or become disabled. Your family keeps the house — period. Often available with living benefits that pay out even if you're still alive but critically ill.

Best For

Homeowners · Young families · Single-income households · Anyone with a mortgage

ANNUITIES

Convert a lump sum into protected, predictable income — often guaranteed for life. Annuities eliminate the fear of outliving your money by creating a personal pension you can never outlive. Ideal as a retirement income foundation.

Best For

Pre-retirees · Risk-averse investors · Pension supplement · Guaranteed lifetime income

Not Sure Which One Is Right for You?

That's the whole point of the review. We look at your situation and tell you exactly what fits — no pressure, no guessing.

Who Needs COVERAGE

IF ANYONE DEPENDS ON YOU,

YOU CAN'T AFFORD TO WAIT.

Insurance isn't about death — it's about protecting the life you've built and the people you love from a financial crisis they shouldn't have to face.

YOUNG FAMILIES

If someone depends on your income, you need coverage now — before something happens. Term life is affordable, fast, and the most impactful financial decision a young parent can make.

HOMEOWNERS

Your mortgage doesn't disappear when you do. Mortgage protection ensures your family keeps the house — without the financial scramble — if the worst happens.

BUSINESS OWNERS

Key person insurance, buy-sell agreements, and executive benefit plans protect your business alongside your family. Your business is an asset — insure it like one.

PRE-RETIREES

Before retirement, the right permanent policy can become a tax-free income source and legacy tool. Waiting costs you — premiums rise every year, and health changes can disqualify you.

SENIORS & FINAL EXPENSE

If you want to make sure your funeral and end-of-life costs don't become your family's problem, final expense insurance is simple, affordable, and guaranteed. No medical exam required.

ANYONE CURRENTLY UNINSURED

You've been meaning to get coverage "eventually." Every month you wait, premiums go up and your health can change. The best time to get insured was five years ago. The next best time is today.

Unsure what you need? One conversation gives you clarity.

WHY YWAIT

AN ADVISOR IN

YOUR CORNER.

Insurance is one of the most important financial decisions you'll make — and one of the easiest to get wrong without the right guidance. We make sure you get it right.

WE WORK FOR YOU.

NOT A COMPANY.

As an independent advisor, Jessica isn't tied to any single carrier. She shops the market to find what actually fits your life — not what earns the biggest commission.

EDUCATION FIRST. ALWAYS..

You'll understand exactly what you're buying, why it fits your situation, and how it connects to your bigger financial picture. No confusion. No fine print surprises.

PROTECTION + STRATEGY. NOT JUST A POLICY.

We look at your insurance alongside your retirement plan, estate plan, and income strategy. Coverage that works in isolation misses half the opportunity.

Clients STORIES

FINALLY PROTECTED.

FINALLY AT PEACE.

"I had a $50k group policy through work and thought I was covered. Jessica showed me my family would have needed at least $600k to replace my income. I had no idea. We fixed it the same week."

Marcus D.

Father of 2, Homeowner

"I was paying way too much for a policy I didn't understand. Jessica reviewed it, found a better fit, saved me money, and actually explained what I had. First time I've ever understood my coverage."

Carolyn T.

Teacher, Age 47

"I kept putting off final expense because I thought it was morbid to think about. Jessica made it simple and compassionate. Now my kids won't have to worry about a thing when the time comes."

Barbara W.

Retired, Age 68

Read more reviews oN Google ↗

Questions

EVERYTHING YOU'VE BEEN

TOO CONFUSED TO ASK.

How much life insurance do I really need?

A general rule of thumb is 10–12× your annual income — but the real answer depends on your debts, mortgage balance, number of dependents, income replacement needs, and long-term goals. The coverage analysis calculates this specifically for your situation so you're not guessing.

What is the difference between Term and Whole life?

Term covers you for a fixed period (10, 20, or 30 years) at the lowest premium — pure protection, no frills. Whole life covers you permanently and builds guaranteed cash value that grows tax-deferred. Term is cheapest for maximum coverage; whole life builds a lasting financial asset. Which one fits depends on your goals.

Is my employer-provided life insurance enough?

Almost never. Most group plans cover 1–2× your salary — far less than what your family actually needs. And when you leave that job (voluntarily or not), the coverage disappears. Employer coverage is a starting point, not a strategy.

What is an IUL and why would I want one?

An Indexed Universal Life policy is permanent life insurance with cash value that grows based on a market index (like the S&P 500) — with a floor so you never lose value in a down year. The cash value can be accessed tax-free in retirement, making it one of the most powerful tools for building tax-advantaged retirement income alongside protection.

Can I get coverage with health issues?

Yes. There are simplified issue policies (health questions, no exam) and guaranteed issue policies (no questions, no exam) designed for people with medical conditions. Final expense insurance in particular is available to almost everyone. We'll find what works for your health situation.

Do I still need life insurance after I retire?

Often, yes. Life insurance in retirement can replace income for a surviving spouse, cover estate taxes, pay for long-term care, or leave a tax-free legacy. Whether you need it depends on your estate, your income sources, and your goals — all of which we review together.

How do annuities work?

An annuity converts a lump sum into a guaranteed income stream — often for life. Think of it as a personal pension you create yourself. It eliminates the fear of outliving your money and gives you predictable monthly income regardless of what the market does.

How fast can I get covered?

Some policies can be approved in minutes with no medical exam. Others with full underwriting may take a few days to a few weeks. We'll match you with the right option for your timeline and health situation.

Can life insurance create tax-free retirement income?

Yes — properly structured whole life and IUL policies allow you to access cash value through tax-free loans and withdrawals in retirement. This is one of the most underused strategies for high-income earners who've maxed out their 401(k) and IRA contributions.

Still have questions? Bring them to the call — we love them.

✓ Free, no-obligation call

✓ Independent — we shop all carriers

✓ Zero sales pressure. Ever.

Helping individuals, families, and unions protect what they've built through estate planning, retirement strategies, and insurance solutions.

619.815.8811

11720 S Foothills Blvd Suite #5, Yuma, AZ, 85367

This site provides general information about legal topics. YWait Agency, YWait Consulting, YWait Wealth Management, and YWait Insurance Solutions are not law firms and do not provide legal or tax advice. Estate Planning Software Licensed from & Powered by Estate Documents Pro.

Legal documents written by Attorneys. Do-it-yourself estate document software licensed from Estate Documents Pro, LLC. This site provides general information about legal topics. ManaEstateDocs.com, YWaitCosulting.com, YWait Wealth and Management, and Estate Documents Pro, LLC are not law firms and do not provide legal or tax advice. This site, and the products available on this site, are not a substitute for the advice of an attorney. You should consult with an attorney and tax advisor licensed to practice in your state for advice if you have questions about your specific circumstances.

© 2026 YWait - All Rights Reserved.